SMM News on June 28:

Metal Market:

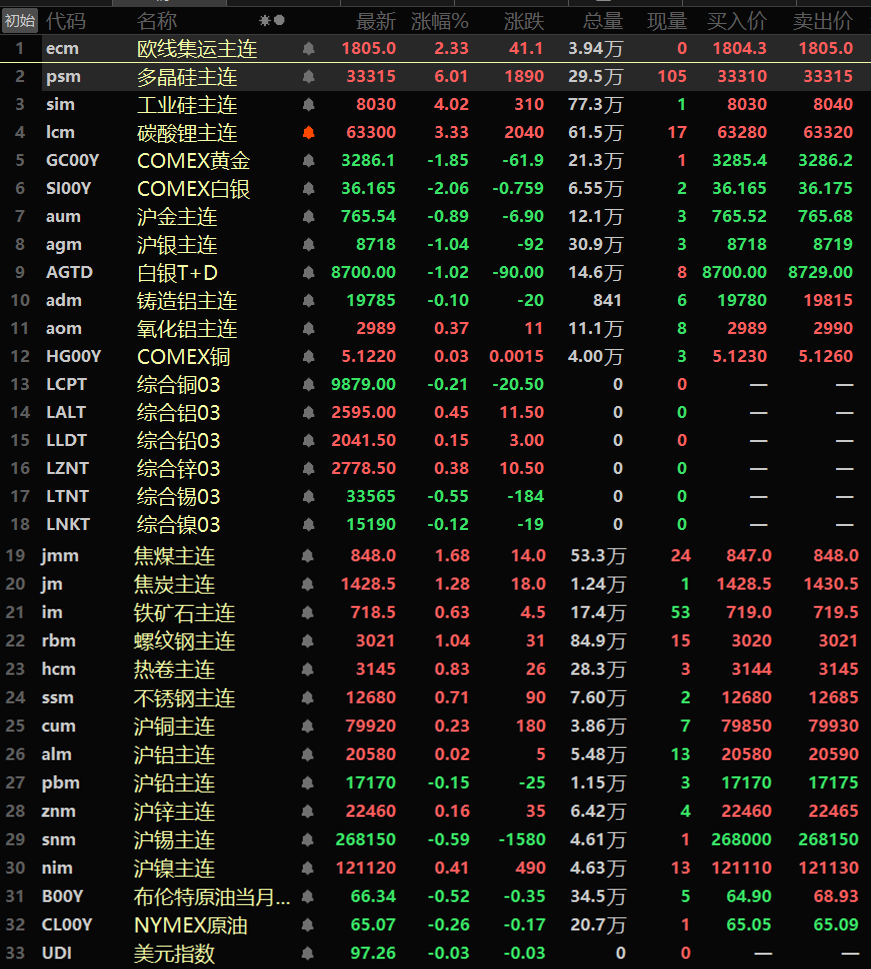

Overnight domestic base metals mostly rose, with SHFE tin down 0.59%. SHFE copper rose 0.23%, SHFE nickel rose 0.41%, SHFE lead fell 0.15%, SHFE aluminum rose 0.02%, and SHFE zinc rose 0.16%. Additionally, the most-traded alumina futures contract rose 0.37%, while the most-traded aluminum alloy continuous contract fell 0.1%.

Overnight ferrous metals series all rose: iron ore gained 0.63%, stainless steel rose 0.71%, rebar rose 1.04%, and HRC rose 0.83%. Coking coal and coke performance: coking coal rose 1.68%, coke rose 1.28%.

Overseas metal markets saw mixed LME base metal performance: LME copper fell 0.21% but posted a 2.55% weekly gain; LME aluminum rose 0.45%, LME lead rose 0.15%, LME zinc rose 0.38%, LME tin fell 0.55%, and LME nickel fell 0.12%.

Precious metals overnight: COMEX gold fell 1.85%, marking two consecutive weekly declines with a 2.94% weekly loss; COMEX silver fell 2.06%, also recording two consecutive weekly losses with a 0.5% weekly drop. SHFE gold fell 0.89% with two straight weekly declines and a 1.88% weekly loss; SHFE silver fell 1.04% but posted a 0.61% weekly gain.

As of 10:29 on June 28, overnight closing prices

》Click to view SMM Futures Data Dashboard

Macro Front

Domestic Developments:

[PBOC: Implement Moderately Loose Monetary Policy, Strengthen Counter-Cyclical Adjustments] The People's Bank of China Monetary Policy Committee held its Q2 2025 (109th overall) meeting on June 23. The meeting analyzed domestic and global economic-financial conditions, noting increasingly complex external environments with weakening world economic momentum, rising trade barriers, divergent economic performances among major economies, and uncertainties surrounding inflation trends and monetary policy adjustments. While China's economy shows positive momentum with sustained social confidence and steady high-quality development, it still faces challenges including insufficient domestic demand, prolonged low inflation, and prominent risk factors. The committee emphasized implementing a moderately loose monetary policy, strengthening counter-cyclical adjustments, better utilizing both quantitative and structural monetary policy tools, enhancing fiscal-monetary policy coordination, and maintaining stable economic growth with reasonably stable prices. 》Click for details

[SSE and SZSE Propose Adjusting Price Limit for Main Board Risk-Warning Stocks to 10%] The Shanghai and Shenzhen Stock Exchanges are soliciting public opinions on adjusting the price limit ratio for main board risk-warning stocks from 5% to 10%, aligning it with other main board stocks. 》Click for details

US dollar:

The overnight US dollar index fell by 0.03% to close at 97.26. On a weekly basis: The US dollar index closed in the red for the week, with a weekly decline of 1.54%. With only one trading day left in the first half of the year, the US dollar has fallen for five consecutive months, set to record the worst first-half performance since 1986. US Treasury Secretary Bessent said earlier on Friday that various trade agreements reached by the Trump administration with other countries may be finalized before the Labor Day holiday on September 1st. According to CCTV News, on June 27th local time, US President Trump posted on social media that the US had just learned that Canada had announced plans to impose a digital services tax on US tech companies. Trump called this a "direct and naked attack" on the US, saying that Canada was clearly following the EU's example. Trump stated that in light of this shocking tax, the US was hereby terminating all negotiations with Canada, effective immediately. The US would inform Canada within the next seven days of the tariffs it would pay to conduct trade with the US.

On the data front, US consumer spending in May unexpectedly declined as the effect of front-loading purchases of cars and other goods before the Trump administration imposed tariffs faded. Meanwhile, US monthly inflation continued to rise at a mild pace. Following the data release, traders increased their bets that the US Fed would cut short-term borrowing costs by 75 basis points in 2025, likely starting in September.

Other currencies:

The euro rose 0.05% against the US dollar to close at $1.1705, touching a high of $1.1754, the highest since September 2021. The euro is on track to achieve a weekly gain of 1.57%, the best performance since May 19th. (Webstock Inc.)

The core consumer inflation rate in Japan's capital region slowed significantly in June, mainly due to temporary cuts in public utility fees such as hydropower. However, the inflation rate remains well above the Bank of Japan's 2% target, keeping market expectations alive for further interest rate hikes by the Bank of Japan in the future. (Webstock Inc.)

RBC Wealth Management stated in its mid-2025 outlook that with the possibility of further inflation pullbacks in the UK, the Bank of England may cut interest rates by a cumulative 75 basis points by the end of 2025. The institution said that UK labour market data appears to be weakening, increasing the likelihood of further interest rate cuts by the Bank of England. However, there is also a risk that stubborn inflation and accelerating wage growth may delay interest rate cuts. London Stock Exchange Group data shows that the market currently reflects expectations that the Bank of England will cut interest rates by a cumulative 51 basis points by the end of 2025. ((Huitong Finance)

Macro Aspects:

Next week, the following data will be released: China's official manufacturing PMI for June, the UK's final annual growth rate of production-based GDP for Q1, the UK's final quarterly growth rate of production-based GDP for Q1, Germany's monthly growth rate of actual retail sales for May, Germany's annual growth rate of actual retail sales for May, Switzerland's official reserve assets for May, Germany's seasonally adjusted unemployment rate for June, the eurozone's annual growth rate of seasonally adjusted money supply M3 for May, Germany's preliminary annual growth rate of CPI for June, the US's Chicago PMI for June, Japan's Bank of Japan Tankan Large Manufacturing Index for Q2, China's Caixin manufacturing PMI for June, France's final SPGI manufacturing PMI for June, Germany's final SPGI manufacturing PMI for June, the eurozone's final SPGI manufacturing PMI for June, the UK's final SPGI manufacturing PMI for June, the eurozone's preliminary annual growth rate of unadjusted harmonized CPI for June, the eurozone's preliminary annual growth rate of unadjusted core harmonized CPI for June, the US's final SPGI manufacturing PMI for June, the US's ISM manufacturing PMI for June, the US's JOLTs job openings for May, Mexico's SPGI manufacturing PMI for June, Australia's AIG manufacturing performance index for June, the eurozone's unemployment rate for May, the US's Challenger job cuts for June, the US's ADP employment change for June, the global ANZ commodity price index annual growth rate for June, Australia's monthly growth rate of imports and exports for May, China's Caixin services PMI for June, Russia's SPGI services PMI for June, Switzerland's annual growth rate of CPI for June, the UK's final SPGI services PMI for June, the US's seasonally adjusted non-farm payrolls change for June, the US's annual growth rate of average hourly earnings for June, the US's non-farm payrolls change in private enterprises for June, the US's unemployment rate for June, the US's trade balance for May, the US's initial jobless claims for the week ending June 28, the US's continuing jobless claims for the week ending June 21, the US's revised monthly growth rate of durable goods orders for May, the US's ISM non-manufacturing PMI for June, etc.

In addition, the following events are worth noting next week: July 1: The Hong Kong Stock Exchange will be closed for one day on July 1 due to the Hong Kong Special Administrative Region Establishment Day, with northbound and southbound trading suspended. July 3: The New York Stock Exchange and the Nasdaq Stock Market in the US will close early at 01:00 Beijing time on July 4 due to the US Independence Day; the trading of stock index futures contracts under the Chicago Mercantile Exchange (CME) will end early at 01:15 Beijing time on July 4 due to the US Independence Day; the US stock market will be closed in the afternoon on July 3 due to the US Independence Day. July 4: The New York Stock Exchange and the Nasdaq Stock Market in the US will be closed for one day due to the US Independence Day; the trading of precious metals, US crude oil, foreign exchange, and stock index futures contracts under the CME will end early at 01:00 Beijing time on July 5 due to the US Independence Day; the trading of Brent crude oil futures contracts under the Intercontinental Exchange (ICE) will end early at 01:30 Beijing time on July 5 due to the US Independence Day; the US stock market will be closed for one day on July 4 due to the US Independence Day.

Additionally, the following events should be monitored next week: 2027 FOMC voting member and Atlanta Fed Chairman Bostic will deliver a speech on the US economic outlook; 2025 FOMC voting member and Chicago Fed Chairman Goolsbee will deliver a speech; ECB President Lagarde will deliver a speech; a panel discussion will be held among global central bank governors (including Fed Chairman Powell, ECB President Lagarde, Bank of England Governor Bailey, Bank of Japan Governor Ueda Kazuo, and Bank of Korea Governor Lee Chang-yong); the ECB will hold a Central Banking Forum in Sintra; the ECB will hold a Central Banking Forum in Sintra; 2027 FOMC voting member and Atlanta Fed Chairman Bostic will deliver a speech on US monetary policy.

Crude oil:

Both WTI and Brent crude oil futures fell overnight, with WTI down 0.26% and Brent down 0.52%. On a weekly basis, WTI crude oil futures fell, with a weekly decline of 11.88% this week; Brent crude oil futures fell sharply, with a weekly decline of 12.11% this week. Earlier reports indicated that OPEC planned to increase production in August, putting pressure on oil prices. After the ceasefire between Israel and Iran, this week's oil price decline marked the largest weekly drop since March 2023.

Four OPEC delegates said that the organization plans to increase daily production by 411,000 barrels in August, following a planned increase of the same magnitude in July. OPEC includes the Organization of the Petroleum Exporting Countries (OPEC) and its allies. If the production increase agreement is reached, it will bring OPEC's supply increase so far this year to 1.78 million barrels per day, equivalent to more than 1.5% of global total demand. However, the group has not yet increased production by the agreed amount, as some member countries are compensating for previous production surpluses, while others need more time to resume production.

The US Department of Energy (DOE) stated that deliveries of crude oil to the Strategic Petroleum Reserve (SPR) will be delayed by seven months due to maintenance. The previous US administration had planned to inject 15.8 million barrels of crude oil into the SPR in the first five months of this year, but only 8.8 million barrels have been injected since January.

US energy services company Baker Hughes said in its closely watched report that US energy companies have cut the number of oil and natural gas rigs for the fourth consecutive month, bringing the total number of rigs to the lowest level since October 2021. Data showed that as of the week ending June 27, the total number of US oil and natural gas rigs, a leading indicator of future production, fell by 7 to 547, the lowest level since November 2021. This represents a decrease of 34 rigs, or 6%, compared to the same period last year. Baker Hughes' report showed that as of the week ending June 27, the number of active US oil rigs fell by 6 to 432, the lowest level since October 2021; the number of natural gas rigs decreased by 2 to 109. (Wenhua Comprehensive)